The space industry has changed dramatically since the Apollo program put men on the moon in the late 1960s.

Today, over 50 years later, private companies are sending tourists to the edge of space and building lunar landers. NASA is bringing together 27 countries to peacefully explore the Moon and beyond, and using the James Webb Space Telescope to peer back in time. Private companies are playing a much larger role in space than they ever have before, though NASA and other government interests continue to drive scientific advances.

I’m a macroeconomist who’s interested in understanding how these space-related innovations and the growing role of private industry have affected the economy. Recently, the U.S. government started tracking the space economy’s size. These data can tell us the size of the space-related industry, whether its outputs come mainly from government or private enterprise and how they been growing relative to the economy at large.

Companies like SpaceX, Blue Origin and Virgin Galactic made up over 80% of the U.S. space economy in 2021. The government held a 19% share of space spending, up from 16% in 2012 – mostly thanks to an increase in military spending.

There are many ways to measure economic success in space.

One way is the economic impact. The U.S. Bureau of Economic Analysis, which tracks the nation’s gross domestic product and other indicators, recently began to monitor the space economy and published figures from 2012 to 2021. The Bureau of Economic Analysis calculated the impact of space using both broad and narrow definitions.

The broad definition comprises four parts: things used in space, like rocket ships; items supporting space travel, like launch pads; things getting direct input from space, like cell phone GPS chips; and space education, like planetariums and college astrophysics departments.

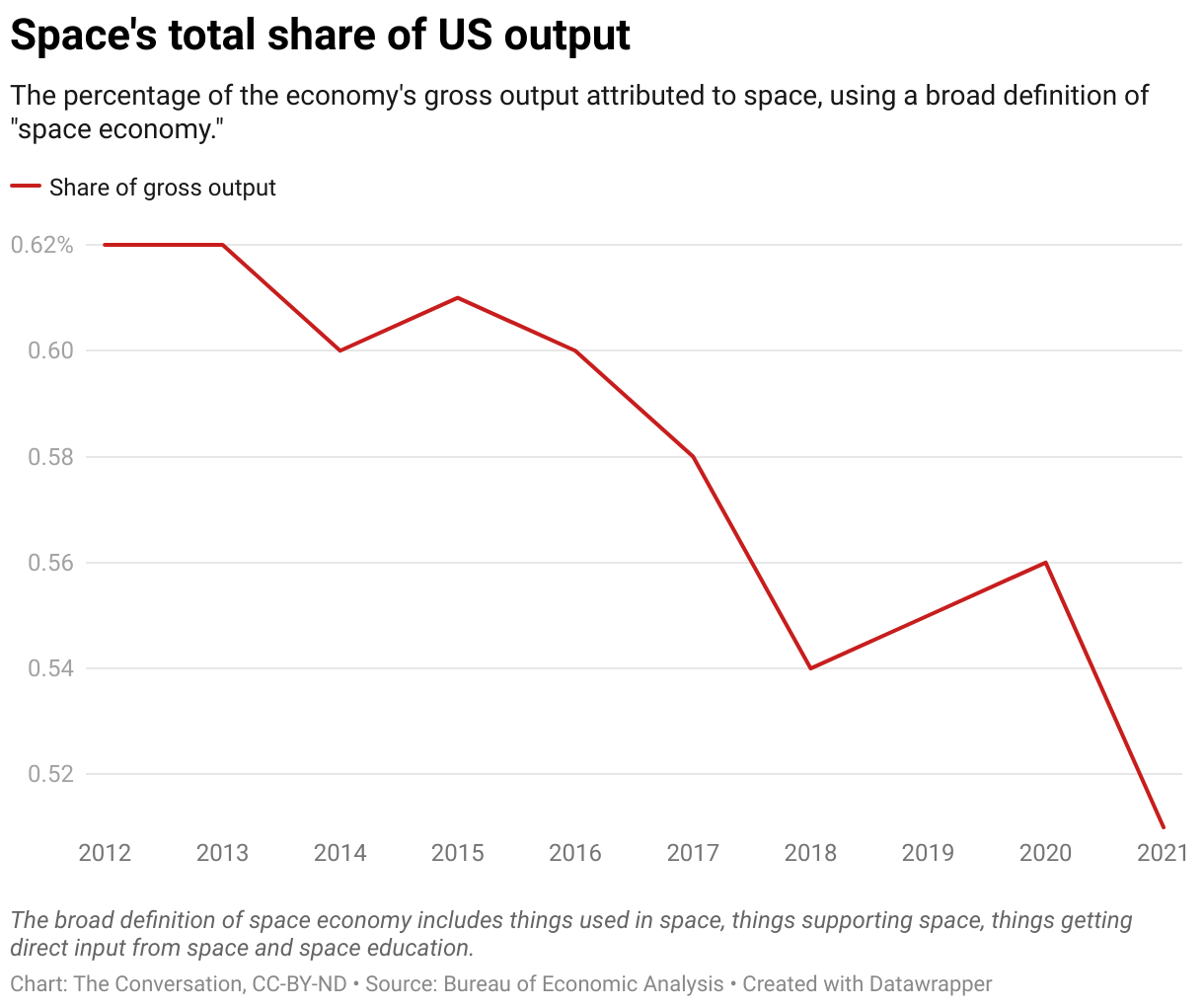

In 2021, the broad definition showed total space-related sales, or what the government calls gross output, was over US$210 billion, before adjusting for inflation. That number represents about 0.5% of the whole U.S. economy’s total gross output.

The Bureau of Economic Analysis also has a narrow definition that excludes satellite television, satellite radio and space education. The difference in definitions is important because back in 2012 these three categories represented one-quarter of all space spending. However, by 2021, they only represented one-eighth of spending because many people had switched from watching satellite TV to streaming movies and shows over the internet.

A closer look at the data shows that space’s share of the U.S. economy is shrinking.

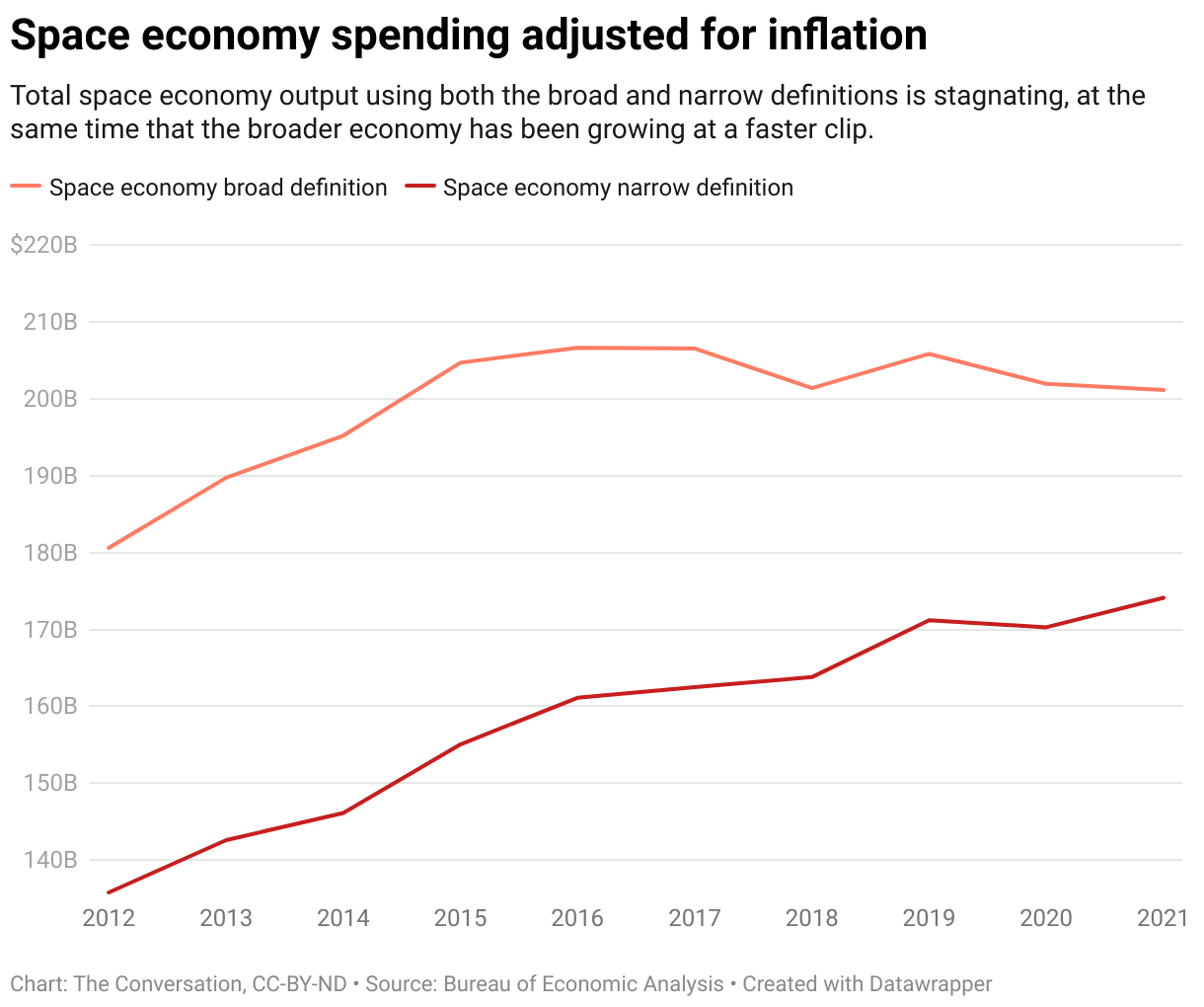

Using the broad definition and adjusting for inflation, the relative size of the space economy fell by about one-fifth from 2012 to 2021. This is because sales of space related items – everything from rockets to satellite TV – have barely changed since 2015.

Using the narrow definition also shows the space economy is getting relatively smaller. From 2012 to 2021, the space sector’s inflation-adjusted gross output grew on average 3% a year, compared with 5% for the overall economy. This suggests space is not growing as fast as other economic sectors.

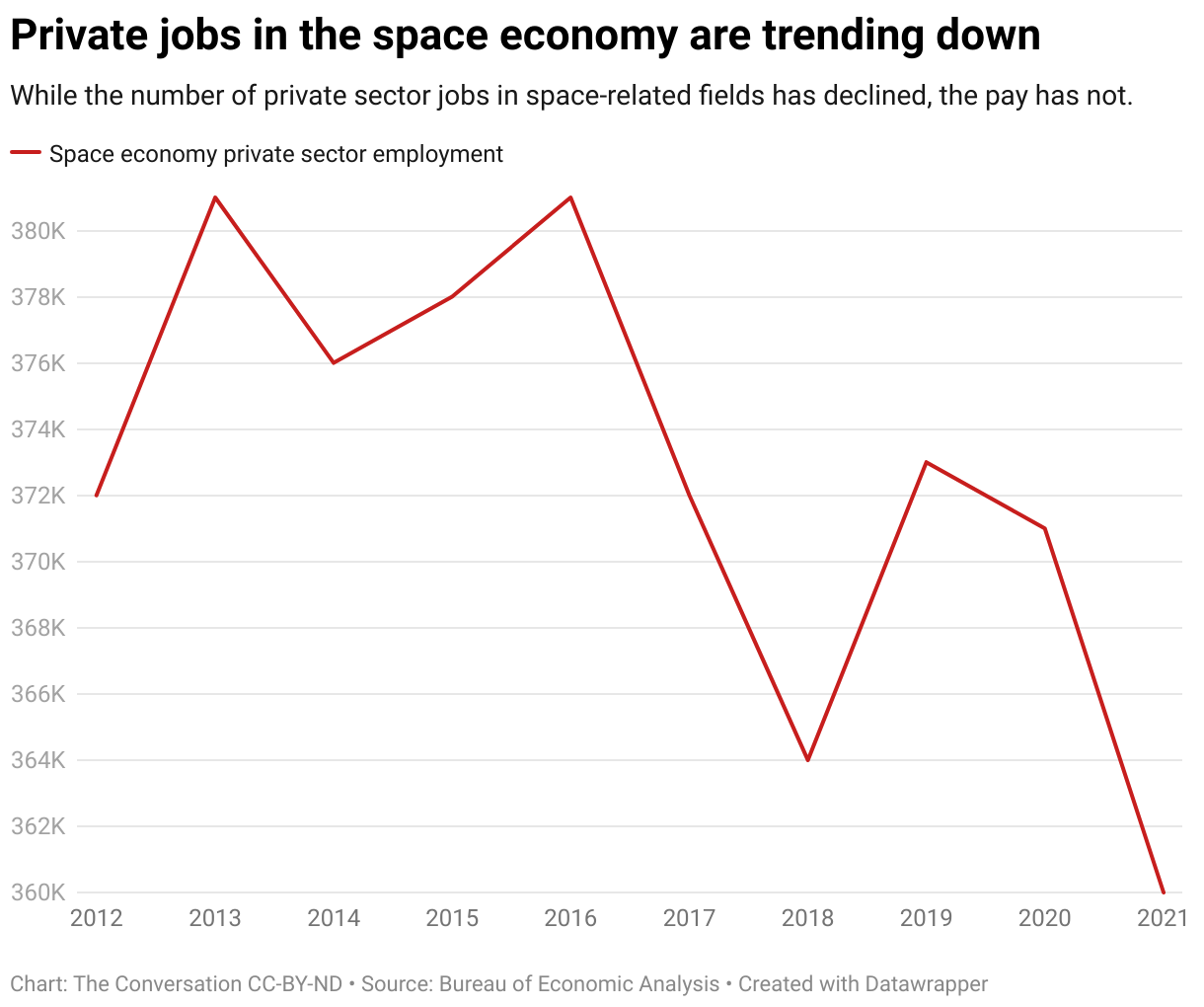

The number of jobs created by the space economy has also declined. In 2021, 360,000 people worked full- or part-time space-related jobs in the private sector, down from 372,000 about a decade earlier, according to the Bureau of Economic Analysis.

The Bureau of Economic Analysis could not track all space-related government jobs since spy agencies and parts of the military don’t provide much information. Nevertheless, they have tracked some since 2018. The military’s Space Force, which is the smallest branch, adds about 9,000 workers. NASA employs about 18,000 employees, which is half of its 1960s peak.

Combining these government workers plus all private workers results in just under 400,000 people. To give some perspective, Amazon’s U.S. workforce is over twice as big and Walmart’s is four times bigger than reported U.S. space-related employment.

The U.S. has long dominated the space economy, especially in terms of government spending.

The U.S. government spent a little more than $40 billion in 2017, compared with about $3.5 billion for Japan and less than $2 billion for Russia.

Moreover, most of the top private space companies are based in the U.S., led by Boeing, SpaceX and Raytheon, which gives the U.S. a leg up in continuing to play a leading role with the rockets, satellites and other stuff needed to operate in space.

The U.S. also published more than twice the amount of space research in 2017 as its next nearest rival – China.

But China is catching up and has narrowed that gap in recent years as top Chinese officials decided success in space is a national priority. Their goal is reportedly to surpass the U.S. as the dominant space power by 2045. China recently put a large space station called the Tiangong into orbit and aims to put people on the Moon.

China’s not the only one joining the 21st century space race. India is expanding its space economy rapidly, with 140 space-tech startups. India launched a rocket on July 14, 2023, that will put a lander and rover on the moon. And the European Space Agency’s Euclid spacecraft plans to map parts of the universe to study dark matter. The ESA released the craft’s first test images at the end of July 2023.

The U.S. has a strong foothold in space. But whether it can maintain its lead – as the space race moves into a new frontier of space mining and missions to Mars – remains to be seen.

This article is republished from The Conversation, an independent nonprofit news site dedicated to sharing ideas from academic experts. If you found it interesting, you could subscribe to our weekly newsletter.

Read more: Returning to the Moon can benefit commercial, military and political sectors – a space policy expert explains Space law hasn’t been changed since 1967 – but the UN aims to update laws and keep space peaceful

Jay L. Zagorsky does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

![]()